What is a start-up? And six other start-up questions answered

There are a lot of questions about start-ups. Here we have provided some of our answers to some of the more common ones:

· What is a start-up?

· What is the difference between a start-up and a small business?

· What are some of the key characteristics of start-ups?

· What are the different phases of a start up?

· What are the roles in a start-up?

· How many start-ups are there?

· How successful are start-ups?

What is a start up?

There’s no agreed or universal definition for a start-up. There are several good definitions by well regarded innovation and disruption leaders:

· Steve Blank (considered by many as the father of innovation in Silicon Valley):

“a start-up is a temporary organisation designed to search for a repeatable and scalable business model”

· Eric Ries, the creator of the Lean Startup methodology:

“A start-up is a human institution designed to create a new product or service under conditions of extreme uncertainty.”

· Serial entrepreneur and CEO and founder of Startups.co Wil Schroter’s definition is:

“A startup is the living embodiment of a founder’s dream. It represents the journey from concept to reality. It is one of the few times when you can take something that is only a dream and make it a reality, not just for yourself, but for the entire world.”

What the definitions have in common is that start-ups:

· Are looking for a new business models

· Want to be scalable and repeatable

· Are searching for a new or different way to solve a problem or provide a solution

· Are thinking big – they want to have a big impact on a market or even the world.

What is the difference between a start-up and a small business?

Both start-up founders and small business owners are entrepreneurs. But they do differ in quite a few ways. Start-ups tend to be looking to disrupt a market or parts of a value chain by looking for new business models or approaches. Small businesses are focused on out-competing existing players and taking share in a market that is normally reasonably well understood. Below some differences between start-up and small businesses across a range of factors – Funding, Business Model, Mentality, Proposition.

What are some of the key characteristics of start-ups?

There are a variety of key characteristics often involved with start-ups:

Solving a problem: A start-up is normally in the early stages of developing a new proposition. Very often they are looking to solve a problem. This may be a problem that very few others have identified. It could be a problem where there are currently solutions that are not particularly good. Typically, the solution to the problem is novel and disruptive. The solution can disrupt the entire market with a new business model or disrupt a part of the value or supply chain with a very different approach.

Using technology: Today, nearly all start ups use technology or several types of technology in combination. The use of the technology can be novel and/or applied in new ways or to markets that have not experienced the technology applied in that way; or at all.

A small team: Start-ups start with small teams. Normally no more than 5 and usually 1-3. Most of the team will have equity in the start-up and they are known as ‘founders’. Often one or more founders will have domain knowledge in the area where the opportunity being explored.

Agility and changes of direction: Start-ups are trying to rapidly validate their idea, build and hone the solution and then move quickly to scale. Very early own, the start-up is trying to ensure it truly understands the problem being solved and the business model or tech application can solve it – differently and better than anyone else. As they search for a solution, they will often change direction or their approach.

Funding: During the early stages, start-ups funding is normally provided by the founding members (and sometimes family and friends). This is often called bootstrapping. Sometimes money is also sourced from family members and friends.

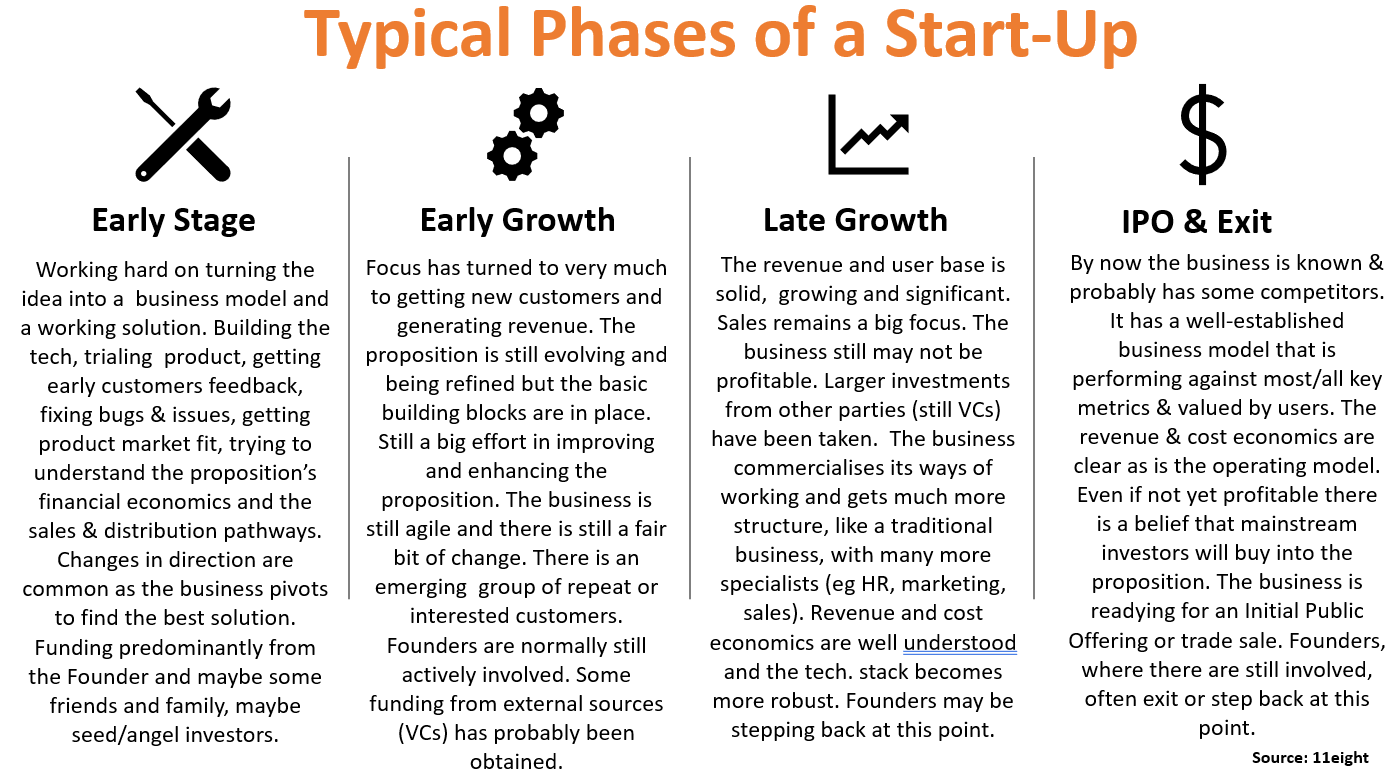

What are the different phases of a start up?

There are many different opinions about the different phases. Often the different descriptions come from start-ups trying to define their stage to help their fundraising efforts. Venture capital firms will use different descriptions to help them clarify the stage of investment they are interested in to support deal flow. Gil Dibner from Angular Ventures in a well-reasoned article considers there are three phases. Some others consider there as many as seven phases - Arsalan Sajid from Cloudways

There is no perfect description, it is helpful to think about the phases by reference to the ‘maturity’ of the start-up - milestones it has achieved, the challenges it is yet to overcome and the things it is focussed on. At 11eight we like to consider four phases of a start-up – see below.

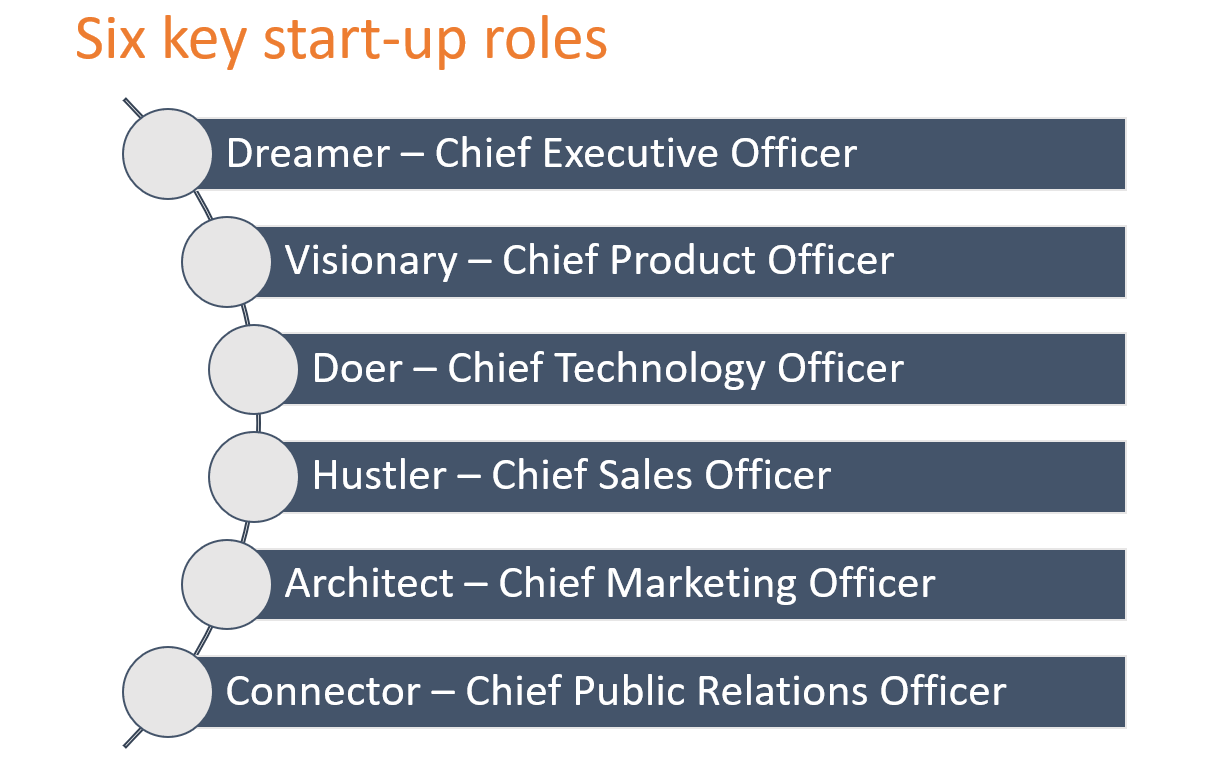

What are the roles in a start-up?

There are many different roles in a start-up. Matt Warcholinski of BrainHub identified six critical roles.

The Chief Executive Officer (CEO) - The Dreamer: Normally the leader of the team and one of the Founders. The CEO’s passion is immense and sees no problem that can’t be overcome and wants to change the world. A great story-teller - the CEO leads and others are willing to follow the dream. The CEO will normally play the key role in raising money when it is needed.

The Chief Product Officer (CPO) - The Visionary: Like the dreamer, the Visionary has a really strong vision for the company and a developed sense of what is needed to convert that vision into a reality. The Visionary can identify the building blocks, anticipate problems, knows who to get over them and has a good feel when something is not going to work.

The Chief Technology Officer (CTO) - The Doer: Every start-up must have that someone who really gets the technology – it is a must have. The CTO must work out the tools and equipment, the hardware and the software, needed to bring the dream and the vision to life; to get the product to market. It is complex. The CTO must be problem solver and be able to anticipate problems, and solve the problems that arise, quickly.

The Chief Sales Officer – Hustler: This person sells the product built by the team – to get revenue flowing in. They open doors, get access and create opportunities, build a rich funnel of sales opportunities and then convert those opportunities into sales. They play a critical role in providing feedback about what customers are saying – the good, the bad and the ugly. This feedback ensures the product is continually refined so it becomes market leading.

Chief Marketing Officer (CMO) – Promoter: The CMO is a story-teller and a gun ‘communicator’ and knows how to orchestrate a message using all the marketing tools. The CMO must raise awareness and interest in the product as far and as wide as possible. They must do it in a way that the product is perceived as offering something unique, something different, something people can’t do without and solving a problem that people want solved. A great CMO transforms a good idea into a phenomenal one.

Chief Public Relations Officer (CPRO) – Connector: The CPRO has great reach and an extensive network. They have access to corporates, media, regulators and influencers. They also know people who can arrange introductions and can help solve problems. The connector helps foster a network of crucial contacts and connections that will help them build relationships with customers and eventually get major investments and help their start-up grow.

Importantly, and particularly in the very early stages when the start-up is small, the Founders often perform more than one role. For instance, the CEO, the CSO and the CPRO while the CTO might also be the CPO. Also, Boards or Advisory Groups can bring some of the other skills to help the start-up.

How many start-ups are there?

According to Get2Growth there are:

· 472 million entrepreneurs worldwide

· 305 million start-ups operating annually

· 100 million new start-ups a year

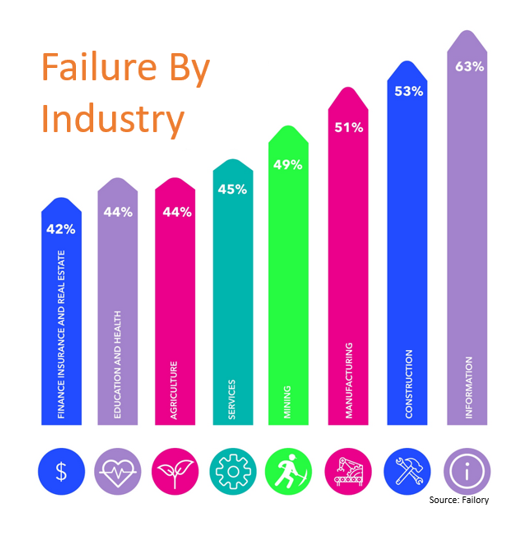

How successful are start-ups?

According to Failory:

· Around 90 per cent of start-ups fail

· Around 10 per cent of start-ups will fail in the first year

· Around 70 per cent of start-ups will fail in years two to five

The failure rate also varies by sector – with finance, insurance and real estate having relatively low failure rates and information based business having comparatively high failure rates